6.2 The method for valuing risk

The value given to a risk in a PSC measures the expected cost of that risk to government if the project were delivered under a public procurement. Once all material risks have been identified and valued, they can then be classified between Transferred and Retained Risks, depending on which of those risks government would allocate to the bidder (Transferred Risks), or which risks government would retain (Retained Risks). These concepts and specifically the risk allocation framework are explored further in both the Practitioners' Guide and Risk Allocation and Standard Commercial Principles.

There are a number of conceptual and statistical methods that can be used to value risk. Broadly, risk can be included in the PSC through one of the following methods:

• including the costs of project specific risk in the cash flow numerator; or

• adjusting the discount rate (cost of capital) to reflect the specific level of risk for each project.

These Guidelines advocate valuing risk in the cash flow numerator of the PSC. The methodology for the determination of the discount rate is provided in Discount Rate Guidance.

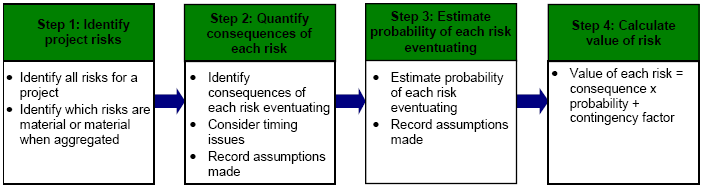

The process of valuing risk can be summarised as shown in Figure 6-2.

Figure 6-2 Steps in valuing risk

The valuation method and level of resources used in valuing risk should reflect a commonsense approach, so that it can be developed and delivered by the procurement team in a timely and efficient manner. This should include a consideration of the expected materiality of the risk to the project, time involved and the costs and resources required to value particular risks. Where appropriate, experienced risk valuation professionals may help to reliably assess the value of risk in a cost-effective and timely manner. This expertise may exist within government, or may be engaged externally.